Getting a mortgage pre-approval is one of the best ways to be successful when shopping for a home. Knowing how much you can afford and what conditions you must satisfy to close your loan are key factors.

Sellers prefer pre-approved buyers because they are a better risk. It doesn’t take long to get pre-approved. Here’s how to go about getting pre-approved for a home loan.

What is a Mortgage Pre-Approval?

A mortgage pre-approval is a statement from the lender stating how much you can borrow based on your qualifying factors.

If you’re pre-approved, it means the underwriter reviewed your credit, income, assets, and employment information to ensure you meet the loan guidelines. The pre-approval is based on an estimated interest rate and will include the required down payment amount.

Consider a pre-approval like someone preliminarily looking at your qualifying factors and telling you if you are approved. For example, it doesn’t consider a property, and most borrowers get a mortgage pre-approval before they look at homes.

How do you get Pre-Approved for a Home Loan?

To get pre-approved for a home loan, you must provide the lender with the following:

A completed loan application with all personal and financial information

Proof of your income which includes your paystubs, W-2s, and tax returns (if self-employed or paid on commission)

Proof of assets to cover the closing costs and down payment

Employer information to verify your employment

Underwriters use this information to determine the following:

What loan program your credit score allows - For example, conventional loans require a credit score of 660+, and FHA loans require a credit score of 580+.

If your debt-to-income ratio fits in the loan program - Most loan programs allow a DTI of 36% - 43%. Your debt-to-income ratio is the percentage of your income that your current (and proposed) debts take up. If your DTI is too high, you could be a risky borrower.

If your employment is stable - Most loan programs require a 2-year stable employment history. Underwriters will evaluate your documentation and get verification from your employer to determine if your employment is stable.

Underwriters evaluate the information you provide. If they have any other questions or need more information, they may make it a condition on your pre-approval letter. While looking at homes, you can gather the necessary documentation to clear the conditions to close the loan faster.

What is a Mortgage Pre-Approval Letter?

A mortgage pre-approval letter is an official documentation from the lender stating that you’re pre-approved for a mortgage.

Being pre-approved means the underwriter evaluated your qualifying factors and determined you qualify for the loan type stated in the letter.

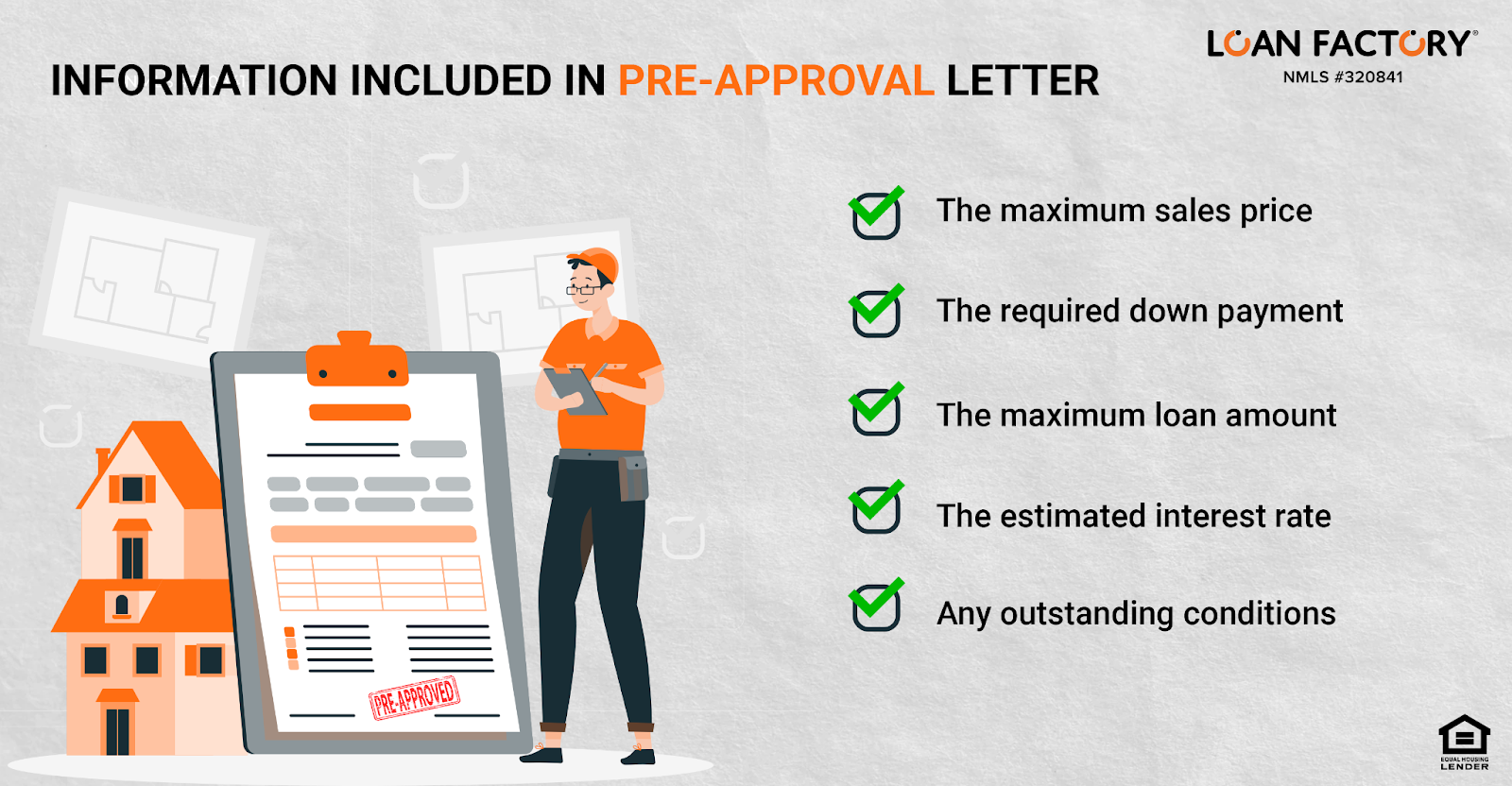

The pre-approval letter will also include the following:

The maximum sales price

The required down payment

The maximum loan amount

The estimated interest rate

Any outstanding conditions

Most lenders will include conditions that you must clear to be able to close on the loan. The conditions always have to do with the property, but there may also be some personal conditions you must satisfy.

A pre-approval letter is usually good for 60 to 90 days. If you don’t find a home before then, you must re-verify the information provided, including your credit score, income, and assets, to prove you still qualify for the loan.

The Benefits of Getting Pre-Approved

Getting pre-approved may feel like a hassle when considering buying a home, but it’s one of the smartest decisions you can make. Here’s why.

Sellers Prefer Pre-Approved Buyers

In a competitive market, sellers may only allow pre-approved buyers to view the home. Even if they allow others to see the home, they won’t accept offers from buyers who aren’t pre-approved. It’s too risky for sellers to pull their homes off the market if they aren’t sure the buyer’s financing will go through.

You’ll Know what you can Afford

It doesn’t make sense to shop for homes you can’t afford. If you receive a pre-approval, an underwriter reviewed your income documentation and can tell you how much you can borrow. Knowing this, you can keep your home search within your price range.

You can Shop Around

You know what a lender will offer you when you have pre-approval. This allows you to compare apples to apples and choose the loan that’s right for you.

You’ll Close Faster

If you’re pre-approved, you’ll close on your home faster once you sign a contract. This is because you will likely have fewer conditions to satisfy, and once the underwriter approves the property with the appraisal and title search, you can close your loan.

Pre-Approval vs. Prequalification

Many borrowers confuse a mortgage pre-approval with a pre-qualification. They are similar but have different outcomes.

A pre-approval means the underwriter pulled your credit and reviewed your qualifying documentation. Then, the lender writes a pre-approval letter, and as long as nothing changes before you close, your personal qualifying factors are approved.

On the other hand, a prequalification is an estimate of what you can afford. An underwriter doesn’t pull your credit or review your qualifying documents. Instead, you work with a loan officer, telling him/her your estimated credit score, income, assets, and debt-to-income ratio. The loan officer uses this information to estimate how much you can afford, but nothing is official because you don’t provide any documentation.

Final Thoughts

A mortgage pre-approval is one of the most crucial first steps when you’re ready to buy a home. So if you are ready to look at what’s available in the market and make an offer, consider getting pre-approved first.

The mortgage pre-approval letter shows sellers you are a serious and capable buyer. It proves you qualify for financing, and if the property passes the requirements, you can close on the loan.

If you’re ready to buy a home, contact Loan Factory to learn how to get pre-approved.